by Striped Giraffe Team

18. May 2026

Reading time: 7 Minutes

The Missing Layer: Product & Customer Orchestration

Growth in finance does not primarily break at channels — it breaks at the point where product logic, customer data, and decisioning fail to meet in one place.

In Part 1 of this series, we examined why digital growth in finance remains inconsistent despite years of investment in digital channels, UX, and onboarding. The conclusion was structural: commercial logic — how products are configured, priced, and exposed — remains fragmented and tightly coupled to core systems.

That fragmentation creates a predictable outcome. Institutions can scale access, but not precision. They can launch digital journeys, but cannot reliably control what offer reaches which customer, under what conditions, and at what moment.

This second part focuses on the missing layer that resolves this tension: product and customer orchestration. Not as an abstract capability but as the operating model that determines whether growth scales or stalls.

Financial products are inherently complex. They are:

- configurable across multiple dimensions (pricing, eligibility, bundles)

- constrained by regulation and jurisdiction

- dependent on lifecycle states (origination, servicing, renewal)

Yet in most institutions, product logic is not governed as a single system. Instead, it is distributed across:

- core banking or policy systems (eligibility, contracts)

- pricing engines (rates, fees)

- CRM platforms (campaigns, segmentation)

- documentation and compliance layers (terms, disclosures)

The result is not just technical fragmentation. It is loss of control.

Where this breaks in practice

A common scenario:

- Pricing is updated in one system

- Eligibility rules remain unchanged in another

- Campaign logic continues to target outdated segments

The institution believes it has launched a new offer. In reality, it has launched multiple conflicting versions of it.

This is not a rare edge case — it is a structural condition. And it directly translates into conversion loss, pricing leakage, and regulatory risk.

Real-world signal

Large European banks have repeatedly highlighted this issue in transformation programs. For example, initiatives around product simplification and catalog centralization — seen in organizations like ING or BBVA — were not primarily about reducing SKUs. They were about regaining control over how products are defined, governed, and distributed.

What leading institutions do differently

They treat product not as a system artifact, but as a governed asset. This typically includes:

- a central product model (single source of truth for configuration)

- explicit control over:

- eligibility

- bundling

- lifecycle states

- pricing logic

- separation between product definition and product execution

This shift has a direct consequence: product changes no longer require system changes.

And that is the prerequisite for speed, iteration, and scalable growth.

Customer data: from marketing view to decision view

Most financial institutions have invested heavily in CRM and CDP platforms. These systems are effective — for what they were designed to do:

- segmentation

- campaign orchestration

- engagement tracking

But they are not designed to support real-time commercial decisions.

They answer: who should we target?

They rarely answer: what should we offer right now?

The structural gap

Offer decisions in finance depend on a combination of inputs:

- risk exposure

- current financial position

- behavioral signals

- regulatory constraints

- consent and data usage rights

These inputs are rarely unified. Instead, they are:

- distributed across risk systems, data warehouses, and operational platforms

- updated at different frequencies

- governed by different ownership models

The result is not just latency — it is approximation.

Why this matters

Without a decision-ready customer model:

- eligibility checks become approximate

- pricing becomes generic

- cross-sell remains campaign-driven

This is why two customers with materially different profiles still receive identical offers in many digital journeys.

Market evidence

The shift toward enterprise MDM and real-time data layers in banking is well documented. Institutions such as Nordea or Deutsche Bank have invested in consolidating customer identity and data governance — not to improve reporting, but to enable consistent, real-time decisioning across channels.

What changes in leading models

A decision-ready customer layer is:

- unified — identity, risk, and behavioral data aligned

- contextual — reflects current state, not historical snapshots

- accessible in real time — usable at the moment of interaction

It is not owned by marketing. It is a cross-functional asset that directly determines commercial outcomes.

Real-time decisioning: where it all converges

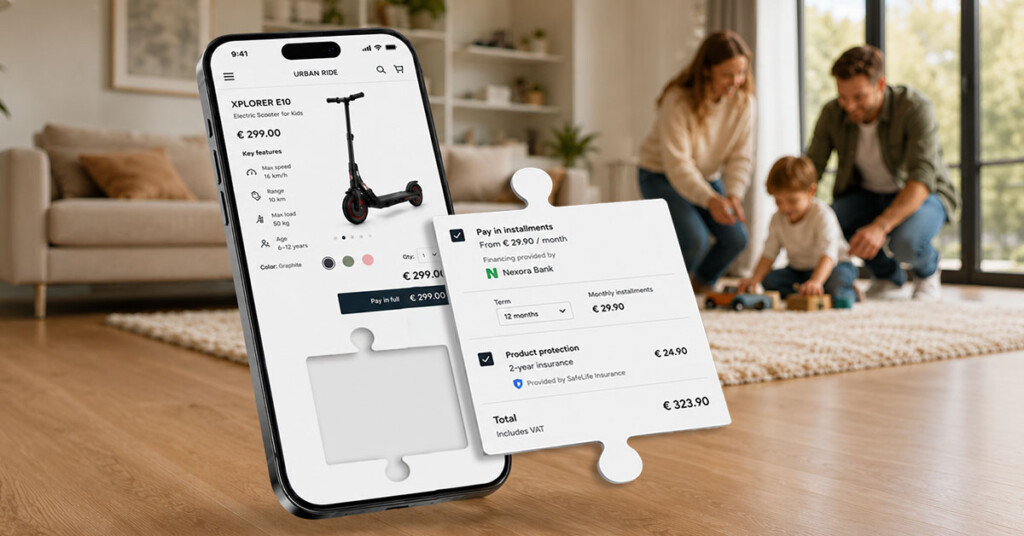

Product governance and customer data only create value when they are connected. That connection happens in decisioning.

Financial offers are inherently dynamic. They depend on:

- who the customer is (risk, behavior, context)

- what the product allows (rules, constraints, pricing logic)

- when the interaction happens (timing, channel, trigger)

This cannot be precomputed. It must happen in real time.

The typical failure mode

In many institutions:

- decision logic is embedded in multiple systems

- batch processes prepare offers in advance

- exceptions are handled manually

This creates:

- latency (offers are outdated at the moment of presentation)

- inconsistency (channels produce different outcomes)

- limited adaptability (new conditions require redesign)

In short: systems are built for stability — not for decisions.

A visible industry pattern

The rise of decision engines and orchestration layers — often discussed in the context of next-best-action frameworks — is a response to this exact limitation. However, when implemented without proper product governance and customer unification, these engines become yet another fragmented layer, adding complexity without resolving it.

What effective decisioning requires

At scale, decisioning becomes a coordinated system where:

- product rules define what is possible

- customer state defines what is appropriate

- risk and compliance logic defines what is allowed

All three must converge in a single execution point. This enables:

- contextual eligibility

- dynamic pricing

- real-time bundling

- consistent outcomes across channels

And critically: traceability.

Every decision can be explained, audited, and adjusted without rewriting core systems.

Closing insight

What limits financial growth today is not access to customers, nor the ability to build digital channels.

It is the lack of control over:

- how products are defined

- how customers are understood

- how decisions are made

Institutions that address these three areas as a unified system create something fundamentally different:

- a governed offer layer

- a decision-ready customer layer

- a real-time decisioning capability

Together, they form the operational foundation for scalable financial commerce.

Growth in finance does not fail at digital channels.

It fails where orchestration is missing.

This foundation is not theoretical. It is tested the moment products leave the institution’s own channels.

In Part 3, we examine how embedded finance and ecosystem distribution expose architectural maturity — and why only a small group of institutions can scale beyond controlled partnerships without losing control of their products, decisions, and compliance.

You might also like:

- From Financial Institution to Commerce Engine, Part 1: Why Digital Growth in Finance Still Stalls » Learn more

- From Financial Institution to Commerce Engine, Part 3: The Real Test Begins Beyond the Bank’s Own Channels » Learn more

- E-Book: Intelligent transformation of the finance and insurance industry » Learn more

- Booklet: Use Cases for Intelligent Transformation in Finance & Insurance » Learn more

- Top 7 challenges of digitization in the financial sector » Learn more

- The Tech Backbone of Subscription-Based E-Commerce » Learn more

- Data Anonymization: Turning Sensitive Information into Strategic Value » Learn more

- Strategic Patterns of IT System Integration » Learn more